Malaysia’s property market, a widely discussed topic amongst many, seems to have lost some of its charms in recent years compared to its decent equity performance in the early to mid-2010s.

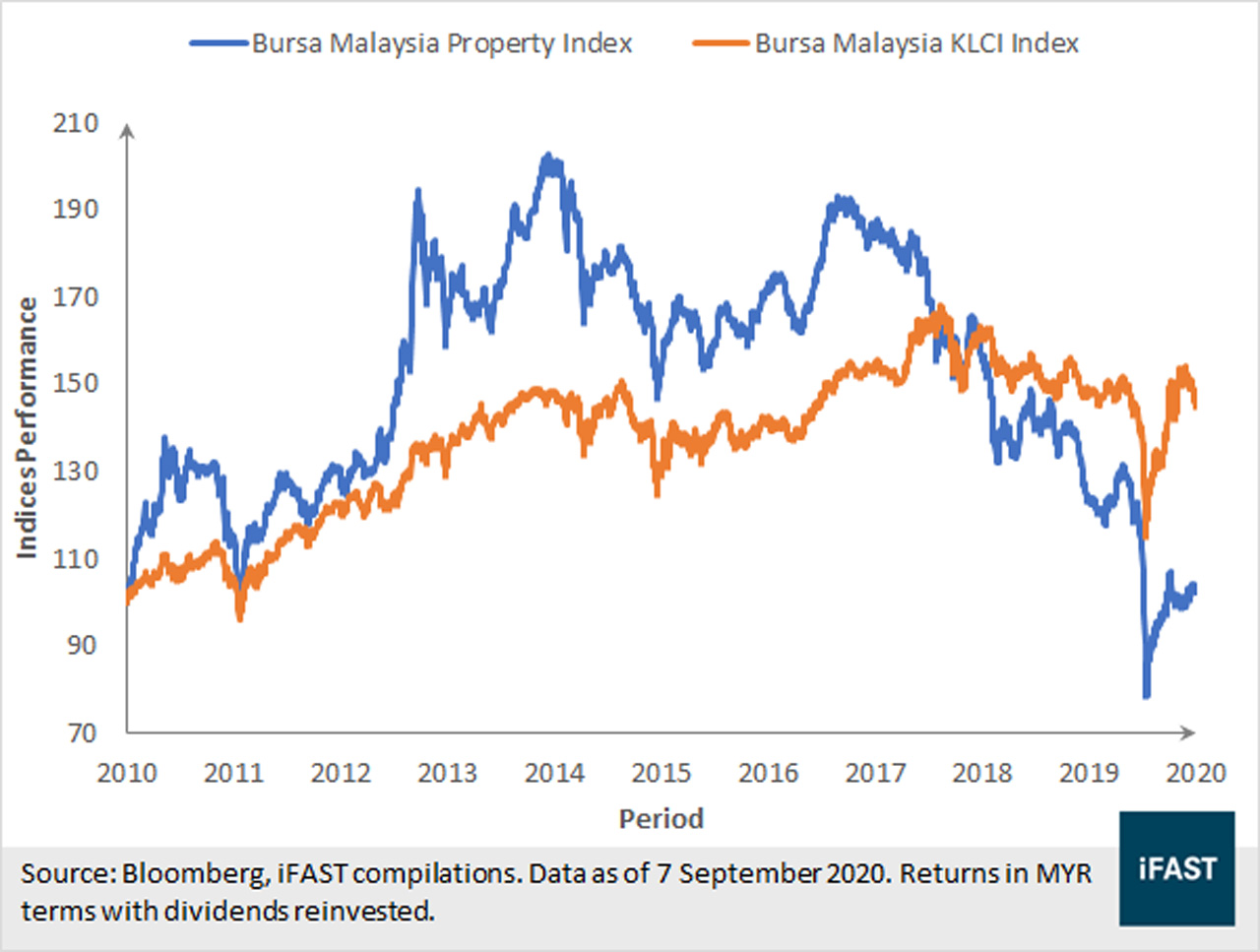

The lack of interest is depicted by the Bursa Malaysia Property Index, as it underperforms the KLCI Index.

In this article, we look to share our thoughts on the local property sector and its prospects going forward.

The Covid-19-19 pandemic has frozen many economic cogs in the country, and the property market has also not escaped from its grasp.

Equities of the local property sector underperform the KLCI Index

The uncertainty of the nature of Covid-19-19 and its duration has held back demand to purchase properties while banks remained hesitant in giving loans especially during the first quarter of the year. This scenario has painted itself in the drastic fall of both loan applied and loan approved in Figure 2 and Figure 3.

However, there are also a few positives that led to subsequent recovery.

Easing monetary policies as displayed by Bank Negara Malaysia (BNM) shaving off 125bps in the OPR has incentivised more demand for high ticket items such as properties.

Moreover, although the almost-complete lockdown of the entire nation has severe consequences, it has greatly reduced the number of Covid-19 infections in the country.

While some of our peers such as Indonesia and the Philippines are still battling with Covid-19 numbering in the thousands daily, Malaysia’s low daily cases have allowed for a gradual resumption in economic activities.

Coupled with the positive development on the vaccine front, consumer sentiment and a demand for properties have similarly rebounded.

A recent example is a launch by Sime Darby Property in Serenia City, Sepang, which has received positive reception with a take-up rate of 100 per cent during the launch period on August 29 to 31.

Demand for loans picking up

Yearly addition in properties remain tepid

Looking towards the supply side of the picture, economic data suggest developers are putting in the effort to control the oversupply that haunts the local property space.

The growth rate of new planned supply, units with building plan approval but have not begun physical construction, is hovering at negative to single digit for the past few quarters.

Lower future supply suggests that the existing stocks available in the market to contract going forward.

The property overhang, properties that are unsold for more than nine months since the launch date, that plagues the local market could remain a thorn to the industry.

The overhang on a country-wide basis in 1Q20 is recorded to be around 33.3 per cent.

Selangor, a state where most developers derive their revenues, has fared better with an average number of 30.4 per cent.

Lower priced properties also have lesser unsold units, which may suggest a pocket of opportunity for developers going ahead.

Recovery similarly seen in approved loans

Governments initiatives to help alleviate pressure from the sector

In light of the challenges caused by the Covid-19 pandemic, the government has highlighted various measures to help businesses and individuals.

The recently announced Economic Recovery Plan (Penjana) has reintroduced the Home Ownership Campaign (HOC), which allows Malaysians to benefit from a minimum of 10 per cent discount and a 100 per cent stamp duty exemption.

The Penjana stimulus has also included the exemption of real property gains tax and the removal of the 70 per cent loan to value ratio.

The greater flexibility provided to buyers is likely to spur the additional sale of properties. Most importantly, these initiatives demonstrate the willingness of the government to support the sector and are unlikely to be reversed going ahead.

During the year, estimated earnings have been on a downwards trend as shown in Figure 8 with a downwards revision by 34 per cent on a year-to-date basis.

Despite such a hefty earnings downgrade, the valuations for the Bursa Malaysia Property Index appear to be inexpensive as of September 7, 2020 especially if valued through the lens of the price-to-book ratio, which is below its 10-year average.

Moving forward, the magnitude of the earnings downwards revision is likely to lose some steam given some of the positives highlighted above.

While earnings will likely take some time to normalise to pre-Covid-19 levels, investors may be compensated through the decent valuations at this current juncture.

All in all, the lackluster equity performance of the Malaysian property sector has been contributed by the challenges faced for the past few years.

While weak earnings appear to be a dragger to the valuations, the record low interest rates, initiatives by the government, and the decent demand for local properties are likely to provide the much-needed support for the sector.

These positives may suggest further downside risk to be limited going ahead.

As such, we are selectively positive towards the sector especially for developers with affordable housing projects which stands to benefit the most from these candies.