Google “Buy vs Rent” and you’ll get hundreds of search results. So, which is better? Both have its strengths.

However, if you are living in Malaysia and are a Malaysian, perhaps the answer is slightly clearer, after you consider factors such as age, and whether you’re a working professional or retiree.

Why it’s better to rent

1. Short-term basis. If you’ve move to a new place because of work and wish to only stay for less than 12 months, it’s better to rent. That’s because viewing, comparing and negotiating successfully for a property to buy takes months, followed by the usual process of applying for a loan and going through the land office. Later when you sell, you’ll have to go through the same processes.

Source: https://www.macrobusiness.com.au/2017/01/2017-demographia-housing-afford...

2. Mortgage slave markets. In some property markets, prices are already very high. Let’s look at below-median household incomes versus the median home prices of the world.

In some countries, buyers must fork out 70% of their monthly salary for a mortgage. For these markets, it’s cheaper to rent.

In Malaysia, if you have to fork out 70% of your salary ONLY for property, it’s unlikely you will get your loan application approved.

3. If there are better investment alternatives. Some people are extremely good with alternative investments. The stock market for instance, where they buy and sell for almost instant profit by studying charts.

There are also those who specialise in commodities like gold and silver, and know the best time to buy and sell.

These people should not tie their money up in property – rather let their money multiply faster elsewhere.

Do take note that cryptocurrency has a much higher risk and is not considered an investment in most countries.

4. Dislike for properties. Many believe property is not as important as cold, hard cash. Truth is, property is also an asset and can also be turned into money.

The downside? It will take a little more time to achieve this.

Why it’s best to buy

1. Property allows us to leverage. Imagine buying a property of RM250,000. We only need a 10% downpayment while the rest is through a bank loan.

In other types of investments, returns are based on how much we invest. For property, the price increase is based on property prices and not how much we invest.

In fact, it may even sound like a scam if someone said you’ll receive double-digit returns every year.

Source: National Property Information Centre (NAPIC).

2. Exciting return on investment (ROI). We buy a property of RM250,000 and pay RM25,000 as downpayment. Let’s assume the price of the property does not increase much, perhaps just 3% per year for the next five years.

This is RM250,000 x 3% x 5 consecutive years = RM289,819 at the end of the five years.

This is RM39,819 divided by RM25,000 (downpayment) = 159%. Divided into five years = 31% returns per year.

Sounds crazy but if we placed the same amount into a fixed deposit account, that will be RM25,000 x 4% x 5 consecutive years = RM30,416.

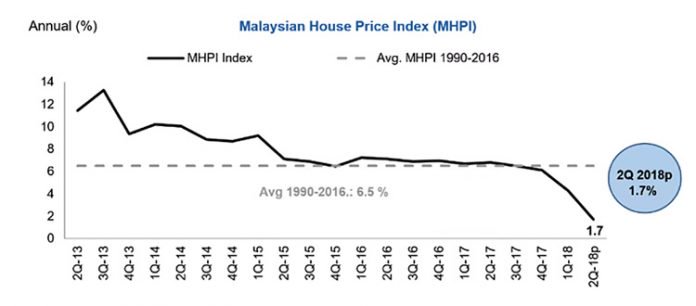

This is a total of RM5,416 after five years. Sad but true. See the chart for the average increase in property prices. (Note: Historical data does not mean the same for the future)

3. Property is a NEED. So buy one that can double up as an investment. A home is not a car. You can choose to take public transport or even pester a colleague for a lift to work every day. However, you cannot sleep under a bridge or stay at a colleague’s home forever.

This is why there will always be demand, and supply will just have to meet demand.

Where price is concerned, let’s understand that MAMEE has been sold at 20 sen for decades. However, the packet size is now many times smaller than previously.

The price of a home may continue to be affordable but the size will become smaller, or developers will build further away.

4. We are Malaysians! Let’s understand that in some countries, the median age is already pretty “high”. So will you buy a new property if you are already 60? The answer is usually no.

However, for Malaysians, we must note that the median age is still 29. So demand will continue to be very strong and if we look at supermarkets, the products with the most choices today are baby products.

5. Property investment is easy. View a unit. Then view a few more. Drive around the area. Are there amenities you like? Look at the developer’s track record. Have they been around for over 20 years?

Compare the prices of equivalent units in nearby neighbourhoods and even cities. We could even look at transacted prices of the properties in brickz.my.

This is unlike many other kinds of investments where the winners are usually just the best in their field or the richest. With property, it’s possible to start with just a right one and move along to the next one.

6. Renting is best when we retire. A prominent individual in real estate once said everyone should aim to have three properties when they retire.

One for own-stay, one for rental income and another they can sell and use the proceeds any which way they like.

Well, why not sell all three and use the proceeds any which way they like? If you choose to travel a lot, renting a place is best.

There are no right or wrong answers.

But truth is, it’s a very good time to rent. There are many home owners who are over-stretched financially and are willing to rent their homes at below market rates just to cover some of their mortgage payments.

This is why some high-rise units in Kuala Lumpur worth RM800,000 may only be rented out at RM2,500 per month today.

However, the question is, how long will this last? Secondly, is it not then the best time to enter the property market when developers are also more willing to have lower profit margins?